Are you a small business owner looking for financial support to fuel your entrepreneurial dreams? If so, understanding SBA loans could be your gateway to success. The Small Business Administration (SBA) has designed these loans specifically to help small businesses overcome financial hurdles, ensuring they have the capital needed to thrive. In this guide, we’ll dissect the essentials of SBA loans, explore their numerous benefits, outline the application process, and address common challenges along the way. Dive in to unlock the potential of SBA loans and pave your path to small business success!

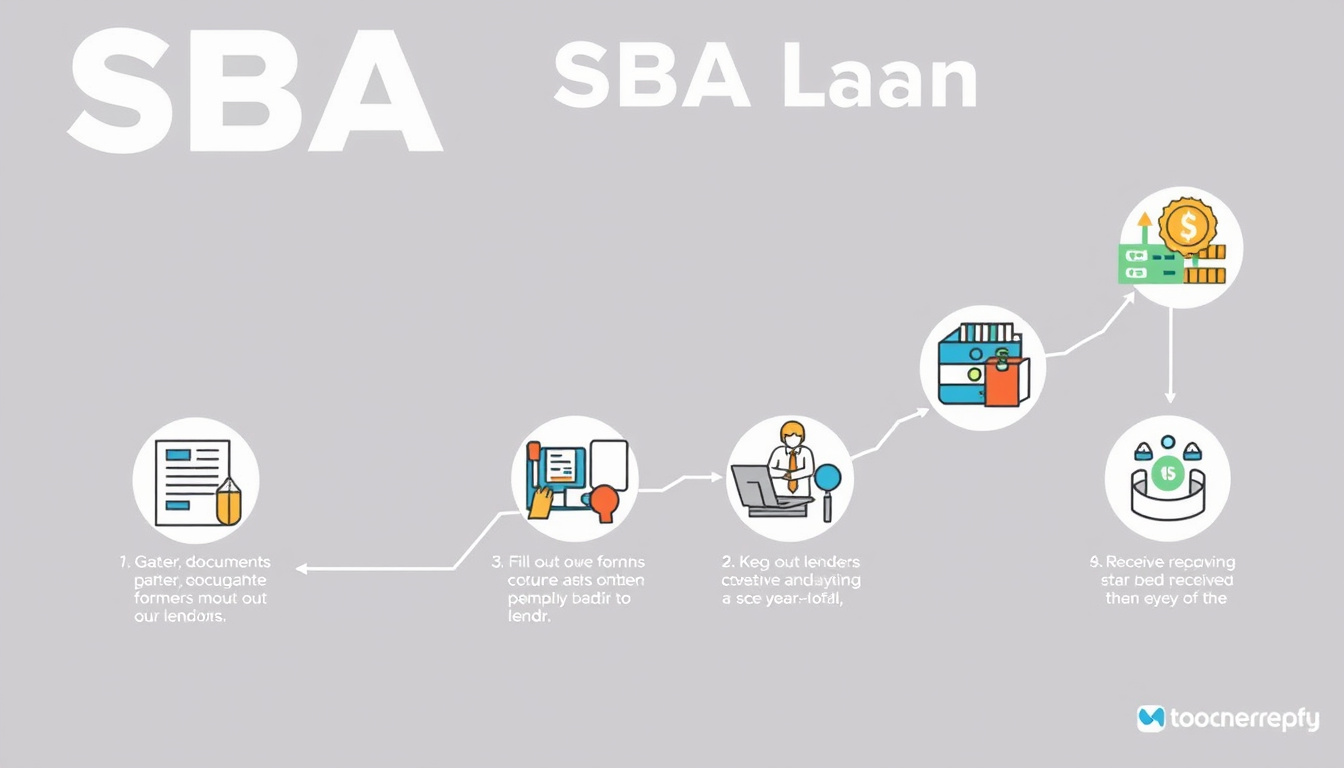

Steps to Applying for an SBA Loan

Navigating the process to secure SBA loans can seem daunting, but breaking it down into manageable steps makes it much easier. First, you’ll need to determine your eligibility, which typically requires being a for-profit business operating within the United States, having a sound business plan, and being unable to obtain financing from conventional sources. Next, it’s crucial to gather all necessary documentation, including financial statements, tax returns, and a detailed business plan. Once prepared, you can then select the right SBA loan program that fits your needs, such as the 7(a) loan for general business purposes or the CDC/504 loan for real estate and equipment. After selecting the appropriate loan type, complete the application process by submitting the required paperwork through an approved lender. Finally, be patient as your application is reviewed, and be ready to respond to any follow-up questions from the lender. By following these steps, you’ll be well on your way to securing an SBA loan to help grow your business.

Common Challenges and Tips for Securing SBA Loans

Securing SBA loans can be an excellent financing option for small businesses, yet many entrepreneurs encounter common challenges during the application process. One of the primary hurdles is the extensive documentation required, which can be overwhelming for first-time applicants. To mitigate this, it’s crucial to be organized and prepare all necessary paperwork in advance, including personal and business tax returns, financial statements, and a well-structured business plan. Additionally, understanding the specific eligibility criteria set by the SBA can help applicants better tailor their submissions. Another frequent obstacle is the need for collateral; many businesses may struggle to provide adequate security for their loans. To navigate this, consider exploring alternative funding structures or seeking advice from financial mentors who can offer guidance on securing collateral or finding lenders that accommodate your needs. Lastly, maintaining a strong credit score is vital; it’s advisable to check your credit history for errors and improve your score before applying, as it can significantly impact your chances of approval. By proactively addressing these challenges and following these tips, entrepreneurs can enhance their likelihood of securing SBA loans and successfully funding their business ventures.

Frequently Asked Questions

What are SBA loans?

SBA loans are loans backed by the Small Business Administration, designed to support small businesses by providing access to affordable financing options. They help small businesses secure funding for various purposes, such as starting new businesses, purchasing inventory, or refinancing existing debt.

What are the key benefits of SBA loans?

SBA loans offer several advantages, including lower interest rates compared to conventional loans, longer repayment terms, and less stringent credit requirements. Additionally, they can help businesses build their credit history and gain access to larger loan amounts.

How do I apply for an SBA loan?

To apply for an SBA loan, first determine your eligibility by reviewing the requirements. Next, prepare your business plan, financial statements, and the necessary documentation. Then, choose a lender that participates in the SBA loan program, submit your application, and follow up to address any questions or concerns they may have.

What challenges might I face when applying for an SBA loan?

Common challenges include lengthy processing times, extensive documentation requirements, and higher approval standards compared to traditional loans. Preparing a comprehensive business plan and maintaining good financial records can help alleviate these challenges.

What tips can help me secure an SBA loan?

To improve your chances of securing an SBA loan, ensure your credit score is strong, create a solid business plan that clearly outlines your business model and cash flow projections, gather all required documentation beforehand, and consider establishing a relationship with the lender prior to applying.

Leave a Reply